TELEFONICA BRASIL (VIV)·Q4 2025 Earnings Summary

Vivo Beats on EPS as Convergence Strategy Drives Record Results

February 23, 2026 · by Fintool AI Agent

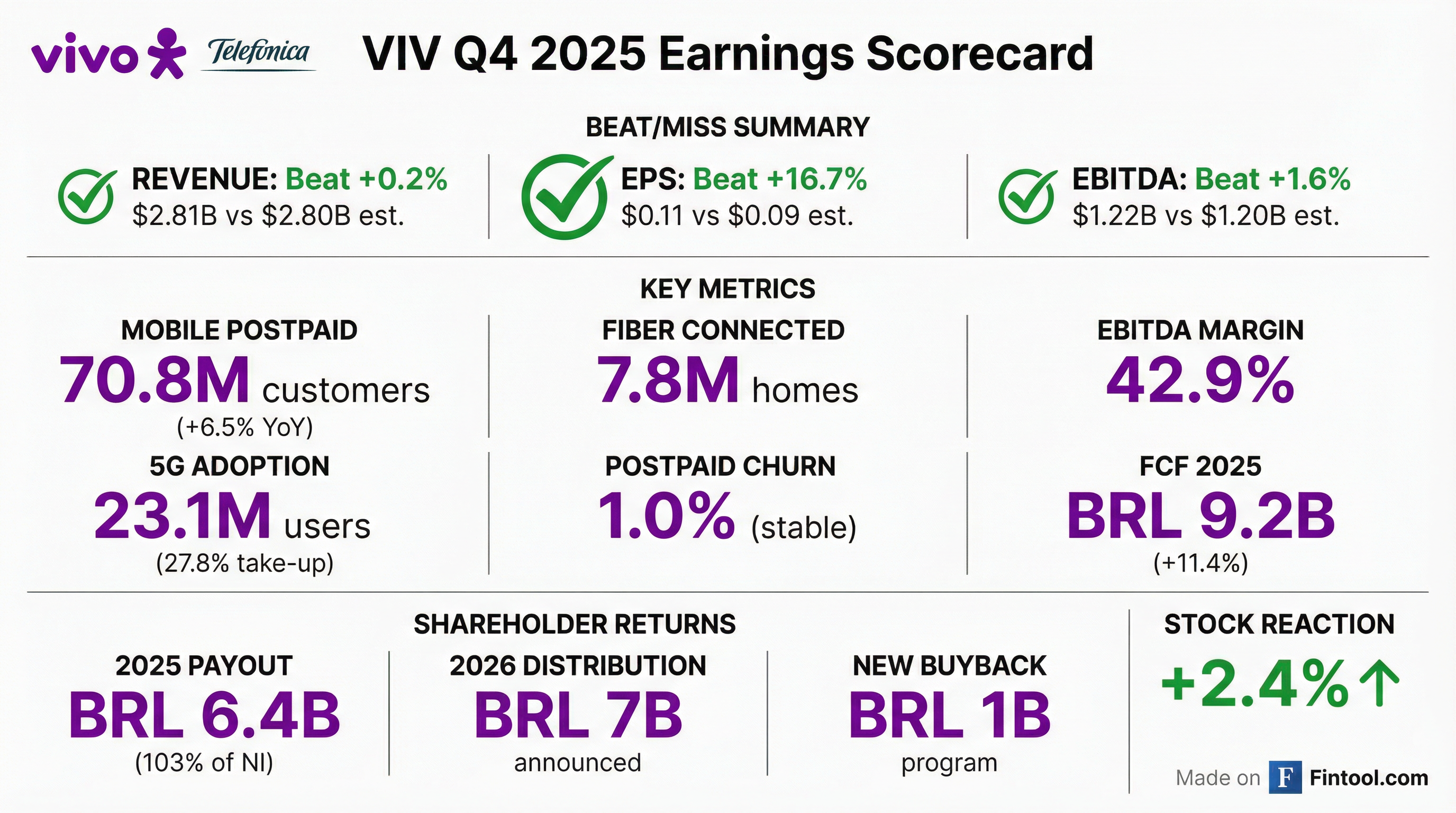

Telefonica Brasil (Vivo) delivered a strong Q4 2025, beating EPS consensus by 17% as its convergent Vivo Total strategy and accelerating digital services drove margin expansion. Full-year net income reached BRL 7.2 billion, enabling a 103% payout ratio. The stock rose 2.4% on the results, touching 52-week highs.

Did Vivo Beat Earnings?

Yes—across all metrics.

Q4 total revenues of BRL 15.6 billion grew 7.1% year-over-year, with mobile service revenue up 7% and fixed services up 5.4%. The standout was reported EBITDA growth of 8.1%—but excluding concession migration effects from both years, EBITDA surged 17.7% YoY with margin expanding 380 basis points to 42.3%.

Historical Beat/Miss Pattern:

Vivo has beaten revenue estimates for 6 of the last 8 quarters, with EPS beats more volatile but significant when they occur.

What Changed From Last Quarter?

Three key developments stand out:

1. 5G Inflection Point — The 5G customer base grew to 23.1 million users across 716 cities, pushing take-up to 27.8% (up 8.6pp YoY). Management noted this "reflects not only the strength of our network, but also the value customers perceive in transitioning to newer technologies."

2. New Businesses Hit 12%+ of Revenue — Non-connectivity services grew 27% YoY and now represent 12.1% of total revenues (up 1.9pp YoY). B2C digital services (video OTTs up 18%, consumer electronics up 36%, health/wellness up ~70%) and B2B digital solutions (cloud up 38%, IoT/messaging up 26%) both contributed.

3. Vivo Total Convergence Acceleration — The flagship fiber+mobile bundle grew subscribers 41% YoY. Now 62.7% of all fiber customers are postpaid convergent, with 43% specifically on Vivo Total. Fiber churn dropped to 1.4%—the lowest in company history.

What Did Management Guide?

2026 Distribution: BRL 7B+

Management announced concrete shareholder returns for 2026:

- BRL 4B capital reduction (payable July 2026)

- BRL 3B interest on capital (payable April 2026)

- Additional interest on capital declared February 2026 (payable before April 2027)

- New BRL 1B share buyback program (through February 2027)

CFO David Melcon reaffirmed the commitment to "distributing at least 100% of net income in 2026, maintaining a clear and disciplined capital allocation strategy."

Net Income Tailwind — Starting Q2 2026, Vivo will fully depreciate legacy assets, generating BRL 300 million in pre-tax profit improvement. Combined with potential interest rate declines (Selic currently at 15%), management is "positive about the evolution of net income" for 2026.

CapEx Discipline Continues — While not providing formal guidance, CEO Gebara noted CapEx/revenues declined from 16.4% to 15.6% in 2025, stating: "The idea is to continue to improve infrastructure, keeping our leadership, but being better in the ratio CapEx over revenues."

Key Operational Metrics

Management Commentary Highlights

On Convergence Strategy:

"When you are Vivo Total, switching costs for customers is even higher. We also have the ability to have a closer relationship with these customers and monetize even better... 84% of the sales that we have of fiber in our stores get out of store with Vivo Total." — Christian Gebara, CEO

On Fiber Market Consolidation:

"The market is still very fragmented... We are the leading company in fiber in Brazil with 19.3%. When I see the leading company in Spain has 34% market share, when I see the leading player in France has 39%, I think there is room for consolidation." — Christian Gebara, CEO

On AI Implementation:

"With Gen AI, the possibilities are even higher. We are using that to optimize internal processes... We're also using AI as copilot to all our call center agents and store agents, and now we are piloting AI agents to answer directly to customers. That's a very important project that we're gonna start having the first results in May this year." — Christian Gebara, CEO

On Capital Structure:

"Today we have also approved a share buyback program of BRL 1 billion... The plan for 2026 is to continue taking advantage of the interest on capital, which is a situation unique in Brazil, together with capital reduction, to maximize the value of shareholders." — David Melcon, CFO

How Did the Stock React?

VIV shares rose +2.4% on earnings day, trading at $16.11—near 52-week highs ($16.47). The stock has appreciated 99% from its 52-week low of $8.09.

The positive reaction reflects:

- Strong EPS beat (+17%)

- Raised 2026 distribution guidance (BRL 7B vs BRL 6.4B in 2025)

- Record-low fiber churn demonstrating convergence success

- Continued margin expansion potential

What's Next? Forward Catalysts

Near-Term (Q1-Q2 2026):

- Price increases: Postpaid/hybrid back book in April, FTTH second increase in June, Vivo Total 100% customer base in April

- Capital reduction payment: BRL 4B in July 2026

- AI agent pilot results: Expected May 2026

- Depreciation benefit begins Q2 2026 (BRL 300M annual)

Medium-Term:

- Fiber M&A opportunities — Management actively evaluating targets as market consolidates

- Tower cost renegotiations — Tenancy ratio of 1.4x in Brazil vs higher global peers suggests optimization opportunity

- Selic rate trajectory — Potential tailwind if Brazil's 15% rate declines

Risks and Concerns

Competition: Management acknowledged a "very competitive market" with some variation in mobile portability. While confident in Vivo's quality positioning, pressure from Claro on TIM was noted.

FX Exposure: Results reported in BRL face translation risk for USD-based investors. The Real's volatility affects reported dollar earnings.

Fiber Fragmentation: The highly fragmented fiber market (Vivo at 19% vs #2 at 8%) creates pricing pressure until consolidation occurs. Several competitors reported negative net adds in 2025.

Data sources: Vivo Q4 2025 earnings call transcript, S&P Global estimates. Stock prices as of February 23, 2026.